The return of inflation, and its impact on major central banks’ reaction functions, has been dominating financial markets since the start of the year. The longer a period of elevated inflation - or at least fear of elevated inflation - persists, the higher the risk that a perceived transitory phenomenon could become permanent. Early on, we had been in the camp of the ‘transitorians’ but as good economists we are continuously challenging our own views. Therefore, here is another look at the current inflation debate. Spoiler alert: we still believe this period will be transitory but the transition period looks longer and wobblier than previously anticipated.

Please see our related article, Inflation in 18 charts for more.

Current inflation dynamics

Headline inflation is currently running at 5% in the US, and 2% in the eurozone. And it won't stop here. In fact, the entire range of possible inflation drivers is currently at work, including higher commodity prices, supply chain disruptions, production bottlenecks, post-lockdown reopening price mark-ups and in the eurozone, the German VAT reversal.

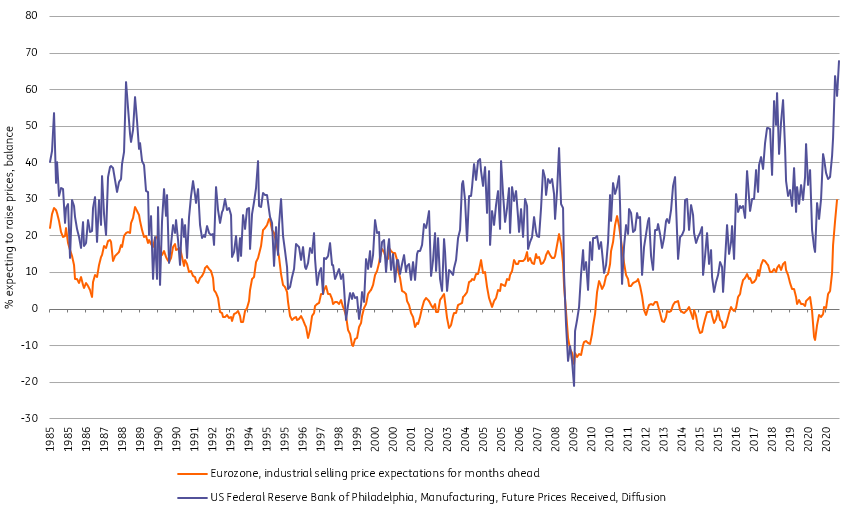

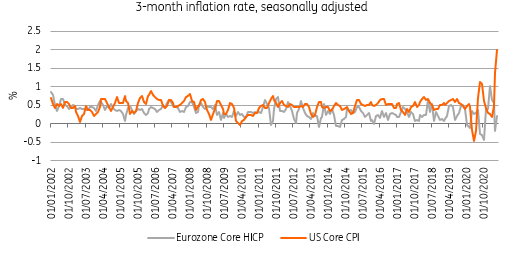

While this cost-push inflation is already in full swing in the US, the later reopening of the eurozone economy, faced with similar global producer price pressures, should lead to an acceleration here in short order. In both the US and eurozone, producer price expectations are close to record highs. With the forthcoming summer holiday season and further reopening of economies, prices in the retail and services space are likely to pick up further. Also, don’t forget that the year-on-year comparison will be one between reopening and lockdowns, accentuating YoY inflation. For the eurozone, inflation is currently still mainly driven by base effects, while the US is already seeing a strong increase in three-month inflation as well.

Recent price growth in the US has been much faster than in the eurozone

Traditionally, it takes between six and twelve months before any pass-through from higher producer prices to consumer prices materialises. There are no standard estimates for this pass-through as pricing power differs depending, for example, on the state of the economic cycle or the level of competition. In the current situation, both in the US and eurozone, high backlogs in the manufacturing sector and cash-rich consumers suggest there is strong potential for a significant pass-through. Add to that the expected jump in prices in the retail space on the back of the coming holiday season and the further reopening of economies, and elevated inflation for the quarters ahead seems all but certain.

Industry price expectations have only shot up very recently in both the US and eurozone

Source: Macrobond, ING Research calculations

All of the above suggests that elevated inflation levels will be ‘transitory’ but this period of transition could be longer than previously anticipated. Even if some of the one-off factors fade out of YoY inflation next year, the delayed pass-through from higher producer prices as well as lockdown-related price volatility could still impact inflation far into 2022. The good news is that credit tightening in China is going to remove some of the pressure on commodity prices towards the end of 2021.

A final driver of inflation going into 2022 could be housing costs. In the US, primary rents and owners’ equivalent rent account for a third of the CPI basket and given that rents are typically only changed once a year, ongoing upward pressure in the housing sector could still show up in the US numbers. In the eurozone, the HICP includes rents but not imputed housing costs. As around 60% of eurozone households are homeowners who don’t pay rent costs, it is fair to say that housing costs are not properly reflected in the eurozone’s inflation measure.

A wage-price spiral in the making?

Major central banks have made clear that they are willing to look through any transitory inflation as there is very little they can do swiftly to stop such inflation and there is still a risk of prematurely choking off the economic recovery. Therefore, all (central banks’) eyes will be on labour markets and wages and any sign of a wage-price spiral.

In the US, employment fell more than 22mn peak to trough, but started to recover rapidly from May 2020. Employment growth has slowed since then with employment still 7.63mn down on pre-pandemic levels. We strongly suspect that recently disappointing jobs numbers are due to a lack of supply of suitable workers rather than any lack of demand. Survey data shows more and more companies reporting vacancies that they couldn’t fill. The lack of supply of workers was also acknowledged in the latest Federal Reserve Beige Book where “a growing number of firms offered signing bonuses and increased starting wages to attract and retain workers”.

There are four main reasons for the lack of worker supply. Firstly, there are ongoing childcare issues surrounding home schooling, which is forcing many parents to stay at home rather than go out to work. Secondly, there is also still some concern from some workers about returning given the pandemic isn’t over. Thirdly, some older workers who lost their jobs may simply have decided to retire early, in part driven by a strong stock market recovery which has improved the financial outlook for retirement. Finally, there is the debate over the impact from extended and uprated unemployment benefits. They may have weakened the financial incentive of going out to work, particularly for low paid roles, especially when you factor in associated costs of commuting and any childcare.

Admittedly, the participation rate in the US is still low and there is the possibility that proposed government policy spending initiatives bring in more workers to fill shortages. Right now there are 1.3mn people who are unable to work, but would like to. There are a further 550,000 people who have been discouraged from seeking work, which could mean they feel as though they don’t have the right skills, or wages are not attractive enough for them to look for work. Finally, there are a further 1.8mn people who are described as not in the labour force, but would like to work and are available to do so now. These may include students who previously worked in bars or restaurants while on campus, but have been unable to given remote schooling. However, as this untapped source of labour accounts for roughly 2.5% of current total employment, it's not likely to prevent wages from rising in the longer run.

Consequently, we may not see labour supply strains ease for another three or four months, which will likely keep employment growth relatively subdued in the near term. This won’t mean demand disappears, merely that those companies that want to expand and grow are going to have to pay more to attract staff.

Average hourly earnings rose 0.5% month-on-month last month versus the 0.2% consensus, which may offer some early evidence of rising employment costs. Note that the 1Q 2021 employment cost index has already shown the strongest increases in labour costs for 15 years, led by the private sector which showed wages and salaries rising 3% YoY with benefits up 2.5%.

Putting it all together, the demand-supply mismatch in the jobs market combined with a political and Federal Reserve aim to make sure as many people as possible feel the benefit of growth – which is only going to happen through jobs and wage growth – we are in a position where we can see some decent wage numbers for once. Federal employees now have a minimum wage of $15/hour and companies such as Amazon have agreed to this, too, even though there is no legislation in place to force them to do so. Certainly, labour supply should become more abundant, but for people out of the workforce for more than a year, skill sets will have deteriorated and the competition for qualified workers will remain intense.

If wages are also now picking up that means costs will rise in tandem, and if companies feel they can pass these on, this too could mean inflation remains higher for longer. Higher wages would also give consumers more spending power. Consequently, a wage-price spiral in the US cannot be ruled out.

In the eurozone, the situation on the labour market is slightly different given the crucial role that furlough schemes have played. We estimate that around 6% of employment was still supported by furlough schemes in March. While the unemployment rate peaked slightly below 9% and has come down to 8% in April, it is only modestly higher than the 7.1% low seen in March 2020, with most of the labour market shock being absorbed by the schemes which were introduced last year and are still running. Slack in the labour market is much higher than unemployment figures suggest.

Following the delayed economic upswing, the lack of skilled workers may be less pressing right now than in the US. Hiring plans have improved recently but remain below historic highs in the manufacturing sector and far below all-time highs in the services sector. With the reopening of retail, hospitality and leisure services, it is possible that the eurozone will also see a temporary lack of skilled employees. However, unless new jobs emerge elsewhere, a return of people from furlough schemes into full-time employment looks like the most plausible scenario. Also, short-term shortages in the hospitality sector could be filled by young people who have been standing on the sidelines of the labour market now for more than a year. Consequently, it is very hard to see any labour market tension like that seen in the US this year.

Looking further ahead, slack in the labour market, and the eurozone economy only returning to its pre-crisis level by mid-2022, are strong arguments against any significant wage growth. Remember that even prior to the crisis when unemployment rates in many eurozone countries were at record lows, wage growth in the eurozone only reached around 2.5%. Still, a soft increase in wage growth should not be excluded given the strong link between inflation and collective labour agreements. Here, direct inflation indexation, as in Belgium, or more indirect or partial indexations, as in France or Spain, play a role. In Germany, unions often bring actual inflation developments into the negotiations. With this in mind, we could see wage growth in the eurozone coming in north of 2%.

Eurozone wage agreements react with a lag on inflation

Longer-term considerations

In our view, the disinflationary period of the last decade was not only the result of the balance sheet recession and subsequent deleveraging and low growth but also a result of two external developments: the emergence of China in the global economy and cheap labour as well as digitalisation (price transparency, competition and making services mobile). In addition to the trends mentioned above, including wage-price spirals and sustainably higher commodity prices, globalisation and digitalisation will also play an important role in the coming years.

Regarding globalisation, it could in fact be more de-globalisation, protectionism and regionalisation of supply chains which push price levels higher. Also, with China’s ambition to become a fully developed economy, the country's role in the global economy could become inflationary rather than disinflationary. Sure, there is still an enormous pool of untapped labour, be it in Africa or Asia, but the question is whether these regions will be able to surpass China quickly or whether this will only come with a long delay. Some economists even claim that the ageing of the global population and the adverse trend of the dependency ratio will result in higher real wages leading to greater inflationary pressure. The disinflationary impact from digitalisation, however, could last a while. Price transparency, increased competition and services becoming mobile have inserted disinflationary pressure on most economies over the last decade and are likely to continue to do so over the coming years. On a different note, it is still unclear how the costs of the energy transition will affect inflation going forward.

It is very early to draw strong conclusions about longer-term inflation trends on the back of the pandemic, but these moves could be far more relevant than most of the transitory factors mentioned above. Changes to underlying inflation trends will not cause large jumps in the immediate outlook, but if indeed a somewhat higher trend in inflation emerges in the aftermath of the pandemic, this would be key for central bank policy.

Implications for Fed and ECB

Almost everything is a matter of perspective. The recent increase in inflation and the future path of inflation are no exception. Indeed, the increase in inflation is mainly driven by one-off factors and therefore transitory. However, the current list of one-off factors is extremely long and varied. Consequently, the risk of seeing pass-through effects and a longer-than-expected period of somewhat stronger inflation is currently the highest since the financial crisis. A pass-through in wages is also possible. To be clear, we don’t see a longer period of accelerating inflation and endless wage-price spirals but rather a longer transitory period of somewhat elevated inflation rates. The probability of seeing such a scenario unfold is definitely higher in the US than in the eurozone. Both the Federal Reserve and the European Central Bank seem willing to not only tolerate temporarily higher headline inflation but also the beginnings of a wage-price spiral. With headline inflation expected to come in at 1.4% in 2023, the ECB clearly belongs in the club of hardcore 'transitorians'. The latest Fed meeting, however, was a good reminder that any forward guidance should be taken with a pinch of salt and that central bankers are sticking with Keynes, who once said: "when the facts change, I change my mind".

Chief Economist, Belgium, Luxembourg

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+