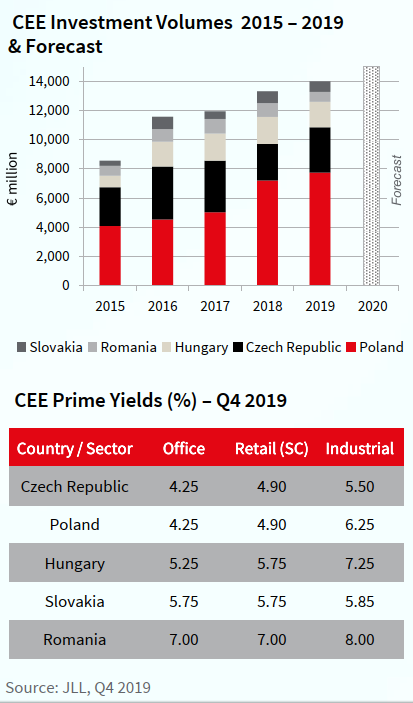

With over 55% of that amount, as well as an increasing activity of the European investors, Poland maintained its dominance among CEE countries. The best result recorded in 2018 was outpaced and consequently the Polish investment market has been growing incessantly for the last several years.

The strong investment activity was also recorded in the Czech Republic. 2019 marked itself with one fourth of all transactions in the CEE and almost 24% increase in the total investment volumes. The market was again dominated by domestic investors. Interestingly, the Asian share of the market, especially the South Korean holds firm at the second position.

Despite the subdued first six months of the year, the investment activity in Hungary improved significantly in H2 2019. Worthy a note is the record-breaking activity within the hotel sector in 2019 overall.

In Romania, 2019 was characterised by rising activity within secondary cities and drop of the total investment volume in Bucharest, the most desired market hitherto. In Slovakia, the investment volume spread evenly between H1 and H2 and 2019. There was also continuous increase of the interest in the retail sector.

Over the last 12 months prime yields saw some downward pressures, with the most visible compressions noted in the office and industrial sectors.

Overall, the CEE investment market is likely to grow further and we may expect 2020 to outperform results registered in 2019.

More information in the attached document by JLL.

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+