____________________________

On March 17, 2021, AmCham Real Estate Council Hotel Market Overview shed some more light on the state and the future of hotels in the Czech Republic. The message was that hoteliers should stay optimistic and that change is inevitable.

AmCham Real Estate Council chair Bert Hesselink of CTP Invest presented results of AmCham Hotel Market Survey, showing that less than 5% of respondents are definite about closure of their hotel. Around 75% of respondents see strong demand from customers to travel. Respondents rate government support at 3 out of 5 (on the scale 1-highest, 5-lowest score).

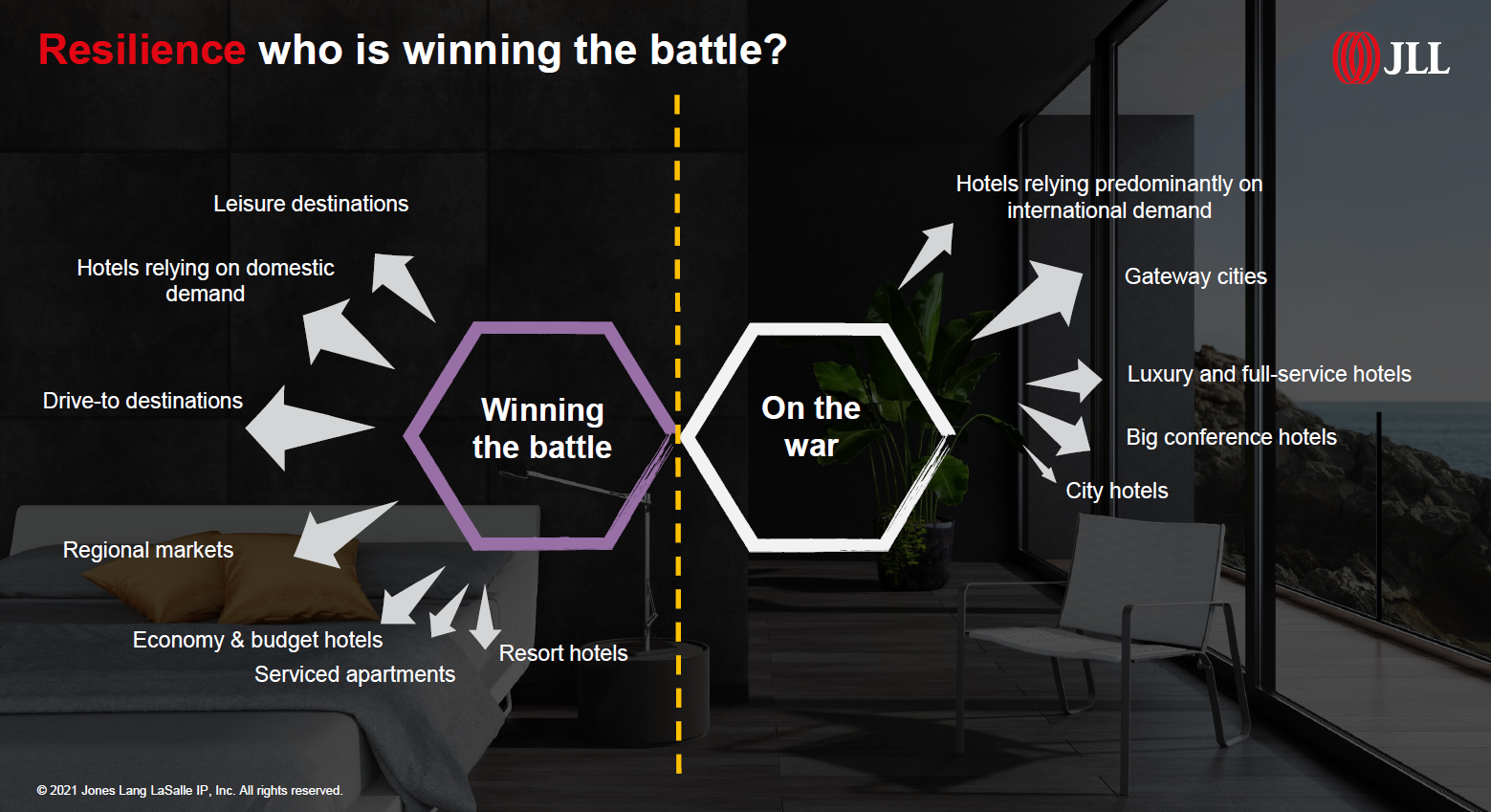

Agata Janda of JLL focused on the CEE perspective. Big gateway cities especially in countries with smaller domestic markets (such as Prague / CZ) are struggling the most because they are heavily dependent on corporate business demand which reduced significantly. Occupancy rates were about 20% in the CEE capitals in 2020. Regional destinations fared better. As soon as lockdown will ease, individual leisure demand is there, but it is rather budget/economy travel. Business travel will return, but in a modified way. Capital movement is currently being seen primarily in the distress area and investors into assets expect a discount. The trend is more residential type of accommodation, focused more on the locals. Two formats have strengthened their position during the pandemic, serviced apartments and open-air hospitality. The line between work, travel, and life is blurring. Hotels will have to adapt to customers who combine these needs.

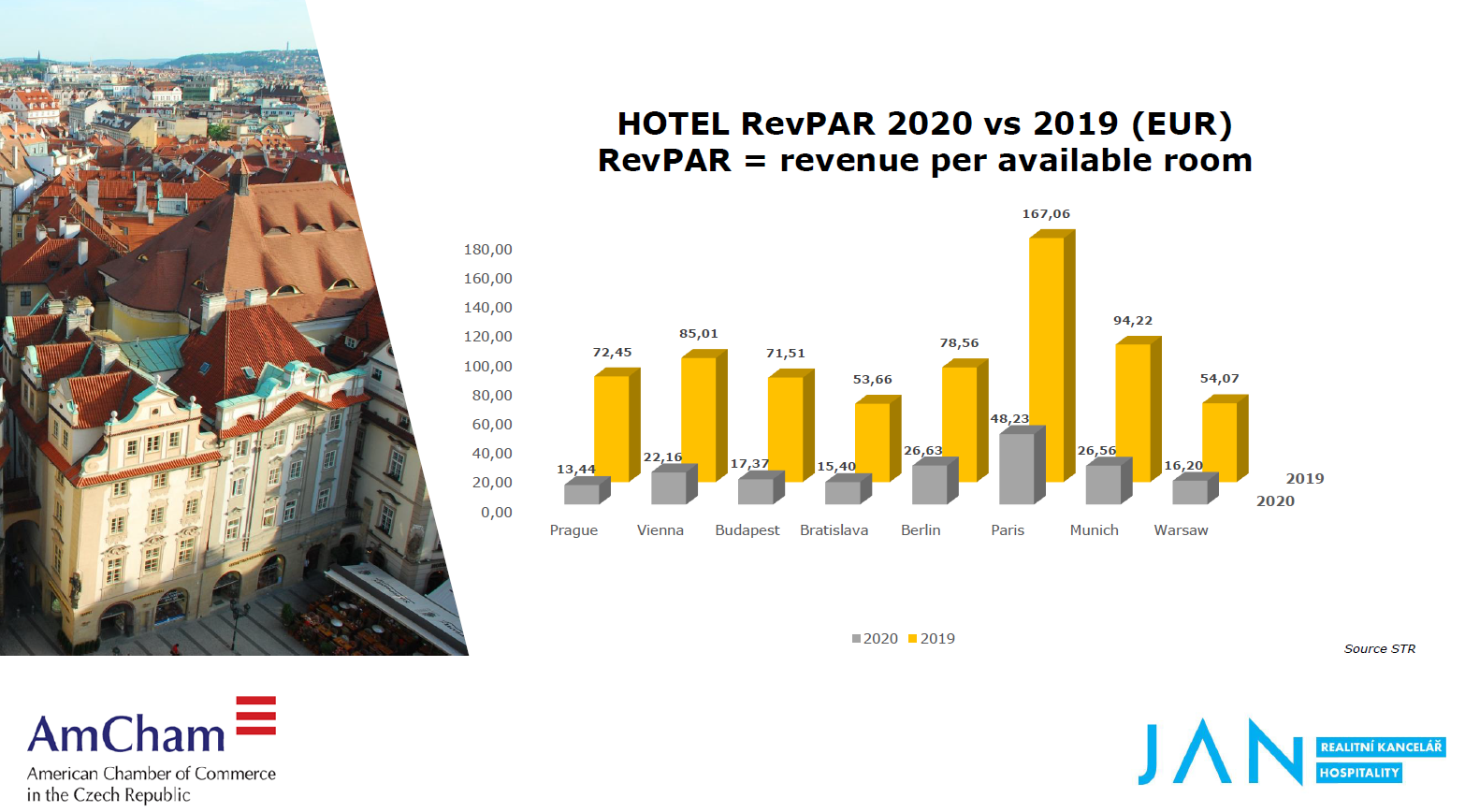

Jan Adámek of JAN Hospitality confirmed that drop of occupancy occurred everywhere, and Prague was hit severely. Average room rate in Prague recorded a drop by 28%. RevPAR is currently at EUR 13.44. Prague Airport recorded 79% drop of passenger numbers in 2020. Increased number of Czech residents staying at Czech hotels in 2020 has not helped most-hit towns and hotels much. In the end, customers will return to hotel chains offering quality.

Hoteliers summed up that currently, the green line is to operate with very little. They focus on limiting costs and surviving, and there are also huge discrepancies between individual cases in the hospitality sector.

Big events had to be moved to 2022 and 2021 will not be as good as expected earlier. The hotel operators who were already barely profitable pre-Covid will struggle the most going forward and this is magnified by the fact that 5-star hotels are selling at the level of 3-star prices which could be another trigger for hotel owners to sell their assets. As for the issue of overtourism, unless the situation with Airbnb is solved, there will never be control over tourism volumes.

According to hoteliers, Government support is absolutely crucial. Cash is what they pay their employees. But with the new planned government support, as the parameters are currently set, it will not be possible to break even.

Prague will stay attractive. The question is how demand will recover and how Prague will deal with it, and what will be the impact on the city as such.

“The ones who are best at managing costs will come out as winners.”

Agata Janda, Director, Hotel Advisory, JLL Poland

Agata Janda, Director, Hotel Advisory, JLL Poland

“The Czech Republic has been struggling a lot, because majority of hotel activity is based in Prague and Prague has a lot of components that made the recovery very difficult.”

“Corporate business demand return may take a while.” Business trips will be less frequent but longer in return.

Jan Adámek, Owner, JAN Hospitality

Jan Adámek, Owner, JAN Hospitality

The ‘real’ tourism will not be back before 2024. "We believe that tourism will never be the same as before." There will be congresses, but some people will attend online. We expect decreased average cost per traveler. "Hotel chains will be preferred, as people will believe in know-how of hotels. Hotel chains will be winners of the game in the end.”

“There is light at the end of the tunnel.”

AmCham Hotel Market Survey (March 2021) was conducted in cooperation of AmCham Real Estate Council and JAN Hospitality.

Full report is available to members.

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+