The report, entitled “Bold Moves in Tough Times” and based on a survey of nearly 500 C-level executives in Europe, North America and Asia-Pacific across 15 industries, found that approximately three in 10 respondents (29%) expect the recovery in Europe to be fairly rapid (“V-shaped”), while 37% anticipate a slower, but steady, “U-shaped” recovery in the next 12 months.

The most optimistic sector is pharmaceuticals/biotech/life sciences, with 34% of business leaders in that sector expecting an increased demand in Europe as a result of the pandemic. The second-most-optimistic sector is communications, media & entertainment, with 52% of those respondents expecting a V-shaped recovery in their European markets, followed by insurance, at 47%. At the other end of the spectrum are the automotive and airlines/travel/transportation sectors, with only 7% and 12% of respondents, respectively, expecting a rapid recovery.

The report also reveals that executives expect the German, Nordic and U.K. economies to rebound the fastest from the downturn, followed by France, Spain and Italy. In addition, European business leaders are optimistic regarding Europe’s competitiveness, as four in 10 respondents (39%) believe that European companies will be more competitive vis-a-vis their U.S. peers than they were before the crisis, and even more (43%) believe that European companies will be more competitive compared with Chinese businesses.

“Confidence is critical in the current economic environment, which is still volatile and uncertain,” said Jean-Marc Ollagnier, CEO of Accenture in Europe. “The optimism regarding Europe’s economic recovery and competitiveness offers European companies a unique opportunity to reinforce their leadership and close the gap with their American and Asian competitors. However, this will depend on how well they translate optimism into bold actions. The biggest risk is that European business leaders remain over-reliant on government support, stay on the defensive and underinvest in game-changing innovations — because their global competition won’t wait.”

Accenture’s research indicates that there is a risk that executives in Europe are overly cautious regarding how they prepare for the rebound, compared with those in North America and Asia-Pacific. Specifically, European executives appear to be:

“Europe’s business leaders must start reinventing themselves for the post-COVID-19 world today,” Ollagnier said. “Now is the time to think and act differently and take balanced risks to build long-term resiliency and to renew growth models to adapt to what we call a ‘never normal’ world.”

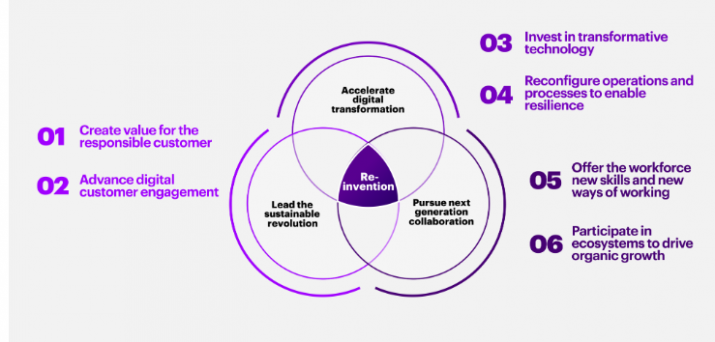

The report highlights critical areas that European companies need to focus on to close the competitiveness gap with their North American and Asian peers. These include:

“Europe is at a crossroads; its business leaders can continue down the well-trodden strategic and operational paths, or they can explore a new way forward, one based on innovation and high-potential technology that blends with Europe’s traditional strengths of sustainability, solidarity and purpose,” Ollagnier said. “Difficult though the COVID-19 pandemic has been, as we emerge from it the scale and scope of new opportunities — particularly in the industrial sector and on energy transition issues — are clear. It’s time for Europe to make bold moves and seize those opportunities to finally close the competitiveness gap.”

About the Research

The research is based on a survey of 478 C-suite executives in 15 countries across 15 industries. The survey was conducted in May 2020 and covers companies with annual revenues exceeding US$500 million. Industries represented include: airlines/travel/transport; automotive; banking; communications/media/entertainment; chemicals; consumer goods; energy; high tech; industrial goods & equipment; insurance; pharmaceutical/biotech/life sciences; public services; retail; software/platforms; and utilities. Countries represented include Australia, Austria, Belgium, Canada, China, France, Germany, Italy, Japan, Luxemburg, the Netherlands, Spain, Switzerland, the United Kingdom and the United States.

About Accenture

Accenture is a leading global professional services company, providing a broad range of services in strategy and consulting, interactive, technology and operations, with digital capabilities across all of these services. We combine unmatched experience and specialized capabilities across more than 40 industries — powered by the world’s largest network of Advanced Technology and Intelligent Operations centers. With 513,000 people serving clients in more than 120 countries, Accenture brings continuous innovation to help clients improve their performance and create lasting value across their enterprises. Visit us at www.accenture.com.

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+