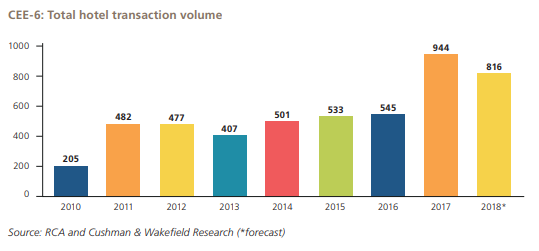

While the total cumulative transaction volume was in excess of EUR 7bn over the 17-year period 2000- 2017, the last five years accounted for nearly 42%, totalling almost EUR 3bn of investment (2013- 2017). The Czech Republic (with Prague already boasting the 10th largest hotel market in Europe), attracted the highest number of investment (38%), followed by Poland (28%) and Hungary (12%), a recently published analysis by CMS and Cushman & Wakefield says.

Transaction activity was especially strong in 2017, totalling a record EUR 944m of investment. This relatively robust volume (73% higher than in 2016), was driven by several major deals such as the Vienna House portfolio (8 properties in Poland, Czech Republic and Romania), the sale of Radisson Blu Complex in Bucharest (EUR 169m), Marriott Prague (EUR 87m), Sheraton Krakow (EUR 70m) or the closure of the 5-hotel portfolio transaction in Budapest by Orbis for EUR 65.9m (Mercure & Ibis hotels). Overall, Poland was the most popular hotel investment market in 2017, followed by the Czech Republic and Romania, which overtook Hungary for third position.

During the Q1-Q3 of 2018, there were fewer major transactions compared to the same period last year. The primary reason behind reduced investment volume in the CEE region is the lack of hotel assets on the market as investors continue to actively scout for deals. There are still large amounts of capital in search for healthy returns, and attention has therefore turned to hotels in CEE that frequently offer superior yields compared to many other regions in Europe and/or other asset classes, the report says.

Infographics credit: Cushman & Wakefield

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+