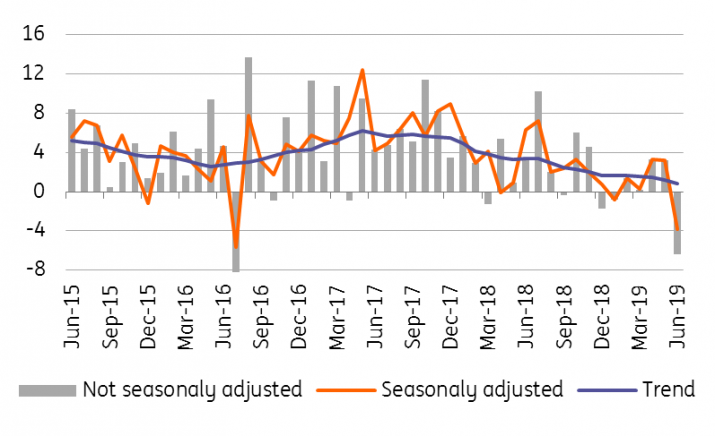

Industrial production fell by 6.4% year-on-year in June after more than 3% growth in previous months. Some of this is related to calendar effects and other one-off factors, but the weaker result is also a reminder that Czech industry is not immune to the German industrial slowdown.

Weak growth in June was partly due to calendar effects, as there was one less working day in the month compared to June 2018. However, even adjusting for this, industry would have fallen by 3.8% YoY, the weakest rate since July 2016, when production was interrupted by holiday shutdowns. In addition to the calendar impact, the higher base from last year also played a role, although the June figure was still significantly below market expectations of -2.6% YoY.

Broad-based slowdown

The industrial slowdown wasn't just driven by manufacturing, which declined by more than 3% YoY (working-day-adjusted), but also by a decline in mining and quarrying (-11%) and energy production (-6.5%) (see chart). Still, there was a noticeable drop in production in almost all the major manufacturing segments, except for rubber and plastic products. Car production fell by almost 8% YoY while in the previous three months growth surprised rather positively, averaging around 5% YoY. Also, new orders fell by almost 10% YoY in June after a favourable April and May, while foreign orders fell by 11% YoY.

Some one-off factors and shutdowns played a role

Although industry was expected to weaken in June, today's result surprised on the downside. In addition to the aforementioned calendar effects and a higher comparison base, some one-off shutdowns in the automotive industry might have played a role, as these were mentioned by some respondents in the June PMI survey. There was probably also some delayed impact from the global manufacturing production slowdown, which until now has been relatively muted in domestic industry.

Stagnation of industry this year

While the June data may appear weaker than it actually is, it's a reminder that domestic industry is not immune to developments abroad and the slowing German economy. Risks from abroad remain significant, which will sooner or later affect the domestic economy. Due to the weaker June, average industrial growth in the first half of this year was just barely positive but based on the recent negative development of leading confidence indicators, stagnation of industry this year would still be a positive result. The June rebound in German new industrial orders provides some small relief, however.

Source, Author: Jakub Seidler, Chief Economist, ING Bank Czech Republic

Source of infographic, data: CZSO, ING Bank

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+