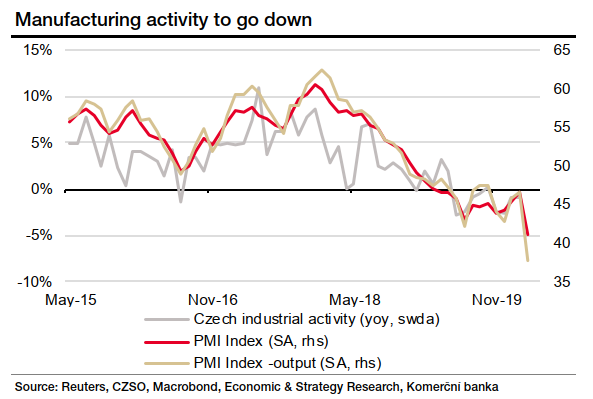

Purchasing manager’s index: Although manufacturing activity declined in March, we expect the bulk of the decline to come in April as companies bore the full impact of economic hibernation and their expectations worsened. Now that the economy has started to awaken again we would expect to see an improvement in the coming months.

Retail sales: Estimating March’s retail sales is a challenging exercise this year. The pandemic has significantly altered consumer behaviour. On the one hand, people have been bulk buying food and drugs but, on the other hand, they have been buying fewer non-essential items. Since mid-March sales have been hit hard by the forced closure of the majority of stores, switching instead to online commerce. We forecast a 4.3% yoy decline in March Czech retail sales, excluding car sales and c.11.5% including car sales, as car registrations fell more than 30% in March.

Industrial production and foreign trade: In addition to the forced decline in activity in many service industries, industrial manufacturers have naturally reacted to mitigate the impact of the pandemic-induced lockdown. From mid-March onward, several key Czech manufacturers, chief among whom carmakers, reduced or completely halted production. As a reminder, in the first half of the month, manufacturers were operating normally. Consequently, for the month as a whole, and adjusting for a theoretical calendar effect of one extra working day, we forecast a drop in industrial production of 12.0%. We expect this to come hand in hand with a fall in exports and lower imports. Declining oil imports and lower consumer demand also point to weaker imports. On the trade balance front, we therefore expect a surplus of close to CZK20bn, i.e. an improvement of CZK4bn.

Czech National Bank: We expect the Czech National Bank to cut its key repo rate by a further 50bp to 0.50% at its regular monetary policy meeting on Thursday, 7 May. This is based on our expectation that growth in foreign demand will recover only gradually, despite the ongoing implementation of government measures to address the impact of COVID-19 on the domestic economy. Our baseline scenario for the rest of 2020 is for interest rate stability, but the risk is concentrated on the side of another rate cut. In 2021, when we expect the Czech economy to grow again, we forecast a gradual tightening in monetary conditions, with higher interest rates and a strengthening of the Czech koruna. However, we expect the koruna to remain weak in the near term, probably below CZK28/EUR. We believe exchange rate intervention would be the most likely way for the Czech Republic to roll out an unconventional monetary policy. However, such as scenario is still a long way off, in our view.

The share of unemployed: Sooner or later, the economic decline will bring about a rise of the unemployment rate. An inflexible labour market and measures supporting the economy hinder a quick rise of the official number of unemployed people. In March, the unemployment rate remained unchanged. At the same time, according to the statistical office, the number of working hours dropped significantly, especially in the case of the self-employed rather than employees. A week before the end of April, the Czech labour and social affairs minister Malacova told the media that the unemployment rate for April would rise to 3.4%. Given the lag of one week, we estimate 3.5%.

Consumer prices: There are several contradictory effects on Czech consumer prices. The decline of oil prices pushes fuel prices lower. Food prices are increasing. With a delay, the weaker CZK is pushing consumer prices higher. The higher excise taxes on tobacco and alcohol have not yet fully translated into consumer prices. We should see a small percentage of that in prices for April, but more should be seen in the inflation reading for May. For April, on average, we expect consumer prices to increase 0.1% mom and a slight acceleration of yoy inflation to 3.5%. The question remains of what quality data has been collected regarding price statistics during the time of economic hibernation.

GDP: Czech GDP is likely to drop significantly in 1Q20 as a result of the coronavirus pandemic. We expect it to decrease 7.6% qoq and 6.3% yoy. This will happen despite the eased monetary policy and supportive fiscal measures. The economic lockdown affected most services and retailers, and also led some manufacturers in the automotive industry to preemptively halt production. As regards the expenditure components, household consumption and investment are expected to weigh on GDP most significantly. The flash GDP estimate for 1Q will be available on 15 May.

More information in the attached report.

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+