The annual publication provides details of taxes paid on wages in OECD countries. It covers personal income taxes and social security contributions paid by employees, social security contributions and payroll taxes paid by employers, and cash benefits received by in-work families. It illustrates how these taxes and benefits are calculated in each member country and examines how they impact household incomes. More.

The Czech Republic Country Profile:

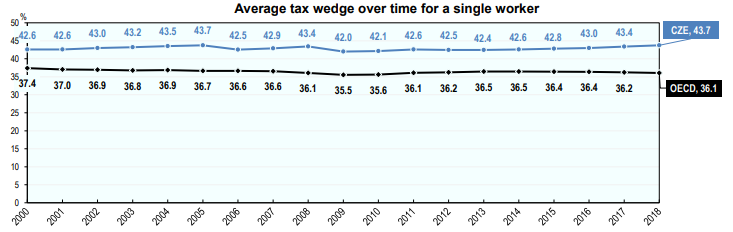

Single worker

The tax wedge for the average single worker in the Czech Republic increased by 0.3 percentage points from 43.4 in 2017 to 43.7 in 2018. The OECD average tax wedge in 2018 was 36.1 (2017, 36.2). In 2018 the Czech Republic had the 7th highest tax wedge among the 36 OECD member countries, occupying the same position in 2017.

In the Czech Republic, income tax and employer social security contributions combine to account for 81% of the total tax wedge, compared with 77% of the total OECD average tax wedge.

One-earner married couple with two children

The tax wedge for a worker with children may be lower than for a worker on the same income without children, since most OECD countries provide benefits to families with children through cash transfers and preferential tax provisions.

The Czech Republic had the 21st lowest tax wedge in the OECD for an average married worker with two children at 25.5% in 2018, which compares with the OECD average of 26.6%. The country occupied the same position in 2017.

Child related benefits and tax provisions tend to reduce the tax wedge for workers with children compared with the average single worker. In the Czech Republic in 2018, this reduction (18.2 percentage points) was greater than the OECD average (9.5 percentage points).

Source: OECD Taxing Wages 2019 report

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+