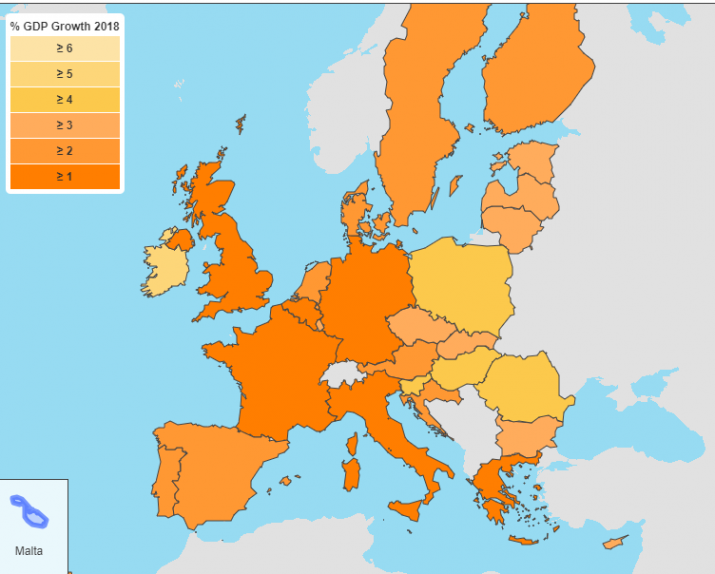

The European Commission published its Summer 2018 Interim Economic Forecast. It covers the years 2018 and 2019 and includes data on gross domestic product (GDP) growth and inflation for all 28 EU Member States.

According to the Commission's forecast, growth is set to remain strong in 2018 and 2019, at 2.1% this year and 2% next year in both the EU and the euro area. However, after five consecutive quarters of vigorous expansion, the economic momentum moderated in the first half of 2018 and is now set to be 0.2 percentage points lower in both the EU and the euro area than had been projected in the spring.

Growth momentum is expected to strengthen somewhat in the second half of this year, as labour market conditions improve, household debt declines, consumer confidence remains high and monetary policy remains supportive.

According to the Commission's forecast, fundamentals remain solid but growth is set to moderate. The fundamental conditions for sustained economic growth in the EU and the euro area remain in place. The moderation in growth rates is partly the result of temporary factors, but rising trade tensions, higher oil prices and political uncertainty in some Member States may also have played a role.

Globally, growth remains solid but rates are becoming more differentiated across countries and regions.

The forecast baseline assumes no further escalation of trade tensions. Should tensions rise, however, they would negatively affect trade and investment and reduce welfare in all countries involved. >> More.

The economy of the Czech Republic expanded by 4.3% in 2017, its second fastest rate in a decade. All demand

components contributed positively to GDP growth. Despite an easing of the pace in 2018-Q1 due to weak

external demand in key trading partners, GDP growth is forecast at a solid rate of 3.0% for 2018 and 2.9% in

2019, thanks mainly to robust domestic demand. The very high confidence indicators readings seen in the first

half of 2018 are fully consistent with these prospects.

Wage increases and high levels of consumer confidence should continue to support private consumption.

Investment is also expected to remain vigorous, underpinned by a revival of construction activity, greater use of

EU investment funding, and a general trend towards industrial automatisation. Meanwhile, public consumption

is set to continue growing at a steady pace, supported by robust wage growth in the public sector.

On the downside, net exports are likely to detract from GDP growth, particularly in 2018. The intensity and duration of this effect will hinge on world trade developments and economic growth in the euro area, particularly in Germany. Labour shortages, which are increasingly cited as a production constraint, also pose a growing risk to the economy. The number of job vacancies was almost twice as large as the number of unemployed persons in 2018-Q1. Continued rapid house price inflation, coupled with rising household debt, also constitutes a vulnerability.

After a temporary slowdown in the first months of 2018, headline inflation is expected to return above 2% in the

coming quarters, influenced by the positive output gap, wage dynamics, and oil prices. The gradual increase of

interest rates by the Czech National Bank, whose latest hike at the end of June raised the policy rate by 25 bps. to

1.0%, should help temper inflationary pressures and maintain consumer price inflation close to the target of 2%.

HICP inflation is forecast to average 2.1% in 2018 and 2.0% in 2019. (Source: EC Summer 2018 Interim Economic Forecast)

Letní #ECForecast: Pro ČR předpokládá Komise pro 2018 růst HDP 3 %, v roce 2019 pak 2,9 %. Inflace se očekává 2,1 % letos a 2 % v roce 2019. Více → https://t.co/r7Kz3OVDw9 pic.twitter.com/FpLouMyjoP

— Evropská komise v ČR (@ZEK_Praha) July 12, 2018

Look also at

Evropská komise dnes vydala letošní přehled zaměstnanosti a sociální situace v Evropě. Zaměstnanost v #EU ještě nikdy nebyla tak vysoká: práci má 238 mil lidi. Výzvou je nyní zejména digitalizace a automatizace. Více o #ESDE2018 → https://t.co/EUOUUph7eF pic.twitter.com/LlKgPTeDsV

— Evropská komise v ČR (@ZEK_Praha) July 13, 2018

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+