Czech economic growth was stronger than expected in 4Q18, mainly due to stronger exports and helped by government consumption. On the other hand, household consumption disappointed, which brings some uncertainty to the outlook. We expect GDP growth to decelerate to close to 2.5% this year, after 3% growth in 2018.

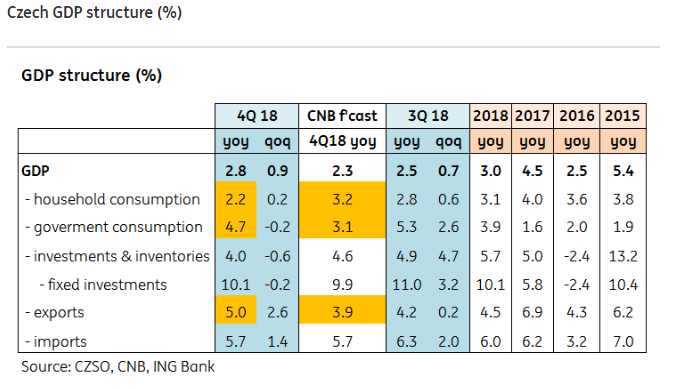

Investments the strongest growth factor in 4Q18

Looking at the detail, the growth in GDP was most driven by investment activity maintaining double-digit growth in 4Q18. In particular, investment in ICT machinery and equipment accelerated (by 13.4% YoY), as companies try to deal with an overheated labour market and workforce scarcity. While infrastructure investment growth slowed slightly, it continued to register double-digit dynamics (12.8% YoY), as did investment in dwellings (11% YoY). Investment in transport equipment decelerated, likely driven by 2H18 emission troubles in the auto segment.

Household consumption weaker

The second most significant growth factor was household consumption. Surprisingly, this slowed to just 2.2% YoY, having grown by over 3% in previous quarters. The slowdown in household consumption was apparent not only in durable goods consumption (possibly also affected by one-offs in the car segment last year), but in all types of goods consumption. Interestingly, wage dynamics slowed from 9.5% YoY in 3Q18 to 7.6%, likely leading to weaker-than-expected average wage growth to be released next week.

Government consumption higher

Government consumption grew more strongly at the end of the year, by almost 5%. The growth in government consumption in the second half of last year was the strongest since 2003 and indicates how expansive fiscal policy was last year. Government consumption contributed 0.8ppt to total 3% GDP growth in 2018.

Better than expected figure driven by net exports

Government consumption aside, the main reason behind the stronger then initially expected 4Q GDP growth was net exports. With total exports growing by 5% YoY, the total negative contribution of net exports to YoY growth was just 0.2ppt. Both ING and the CNB expected a more significant negative impact, -1.2ppt in the case of the CNB.

GDP details sent mixed signals

The structure of GDP growth in 4Q18 brought some mixed signals. While the GDP details confirm solid investment growth, the better than expected print was mainly due to surprisingly strong exports which are likely to decelerate this year on weaker foreign demand. Also, household consumption ended below expectations, suggesting that households are becoming more concerned about the economic outlook. Although the stronger than expected GDP growth, coupled with higher inflation, has led the market to believe that the CNB will raise rates at its March meeting, the current GDP does not signal any imminent need to hike during the next monetary meeting. CNB Board members might prefer to wait for May to have a new forecast in hand, in our view.

Author: Jakub Seidler, Chief Economist, ING Bank Czech Republic

Image credit: ING Bank Czech Republic

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+