Food prices remain high

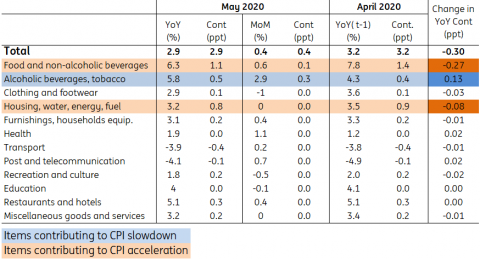

In May 2019, inflation accelerated due to soaring food prices. Due to the high base effect, the year-on-year growth rate of food prices slowed from 7.8% in April to 6.3% in May this year, despite the fact that food prices continued to rise month-on-month - by 0.6%, as in April. The rise in food prices thus remains high, driven by a combination of factors ranging from drought, a weaker Czech koruna and harvest problems in some southern European countries affected by the coronavirus. For example, fruit prices rose by almost 8% in May. From a year-on-year perspective, they are higher by 25%.

Mixed CPI forces in May

As in previous months, the slowdown in price growth from last year was also driven by fuel prices. They fell by around 4% MoM, but their year-on-year decline intensified from 17% to 22%. However, the overall contribution of prices in the transport category did not decrease much, as car prices rose by 1.8%, mainly due to second-hand cars.

The higher than expect monthly increase in prices was driven mainly by higher prices of alcoholic beverages and tobacco, prices of tobacco products increased by 3.7%, spirits by 3.3% and beer by 3.4%.

The CPI slowdown in May was also expected due to a reduction in VAT for selected services, but this effect was not very noticeable. Interestingly, service prices continued growing in MoM terms and YoY dynamics remained at 3.3%.

Structure of inflation in the Czech economy

Deflationary risks seem muted so far

Despite a slight slowdown in annual inflation in May, price growth was higher than expected. Surprisingly, the coronavirus pandemic has not yet resulted in a faster decline in service prices. However, this may also be related to the fact that the measurement of prices in recent months has not been carried out in the standard way and thus may not have captured price developments correctly. While price growth was stronger in May on a monthly basis, we still expect inflation to slow to 2.5% on average this year. The pro-inflationary risks are a weaker koruna and potentially more expensive food prices while fuel prices and prices affected by Covid-19 issues could go in the other direction. How significantly the current coronavirus crisis affects inflation is relatively uncertain.

Unconventional monetary measures not in the pipeline

For the time being, domestic inflation is not showing a significant slowdown and the risk of deflation seems to be remote, although many countries are approaching this scenario due to the crisis. Stronger deflationary risks would probably push the Czech National Bank to act and adopt more non-standard monetary policy instruments, but current inflation figures suggest that this scenario is still relatively far away, in our view.

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+