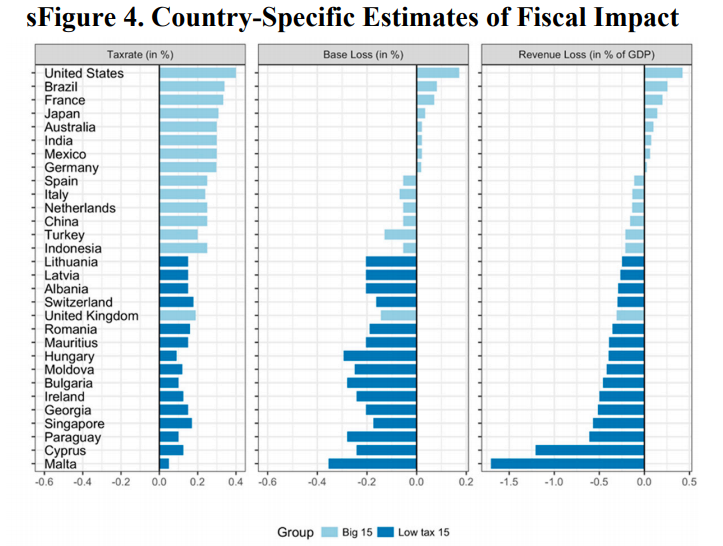

According to a recent IMF working paper on tax avoidance, called International Corporate Tax Avoidance: A Review of the Channels, Magnitudes, and Blind Spots, a 1 percentage point larger tax rate differential reduces reported pre-tax profits of an affiliate by 1 percent. The authors believe that this estimate is larger than the consensus so far and the semi-elasticity has increased over time; a value of around 1.5 applies to the most recent years.

"The insight is extremely important for the policy debate on profit shifting and for the calibration of models that account for tax avoidanc," the report says. Using this estimate, the authors illustrate the revenue impact of tax avoidance for 81 countries.

The graph below shows that seven large economies actually gain from profit shifting because their rate is lower than those prevailing elsewhere:

Source: IMF - International Monetary Fund, International Corporate Tax Avoidance: A Review of the Channels, Magnitudes, and Blind Spots

Members of the American Chamber of Commerce in the Czech Republic

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+