Economic policy / Tax & Finance

This section reports on economic policy initiatives of the Czech government, the EU, and other entities that have a direct impact on the competitiveness of the country. It also includes information on economic priorities of the AmCham and other leading associations.

Show subcategories ▾

Spotlight issue

Amcham´s comments to Act on Digital Tax (3rd reading in Parliament)

We write to express our concerns over the adoption of a Czech Digital Tax on a targeted group of companies that provide the platforms for the creation and international growth of innovative business.

View more

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+

AmCham Intel: AmCham members discussed the current and future tax policy with the Ministry of Finance

AmCham policy update and outlook with the Ministry of Finance representatives Stanislav Kouba, Director General, Section Tax and Custom and Zdeněk Hrdlička, Director, Department for International Tax Cooperation and Relations focused on the current business related issues.

View more

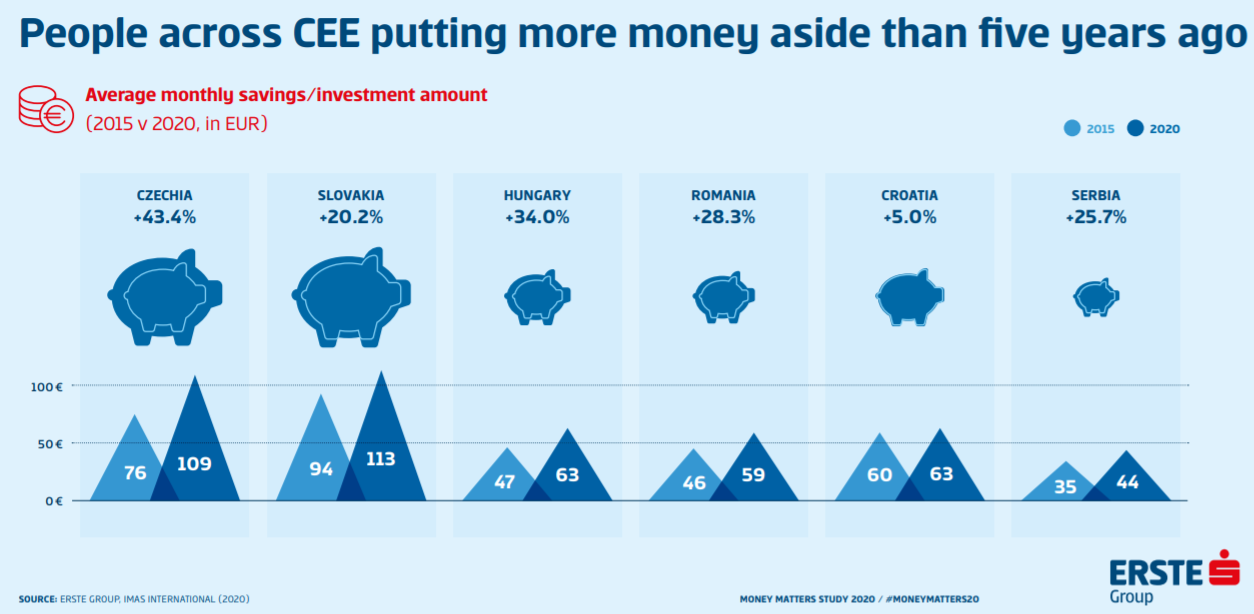

Piggy banks grow fatter in Central and Eastern Europe in Covid times

Average monthly savings and investment volume rose in all CEE markets in 2020, continuing uptrend over past five years

Across region, increasing importance attached to putting money aside, but level of satisfaction with savings and investments varies widely

Key drivers for putting money aside: “rainy days”, planned purchases and safeguarding for old age

Widespread popularity of traditional products like savings books and building savings also reflects risk aversion among CEE savers

View more